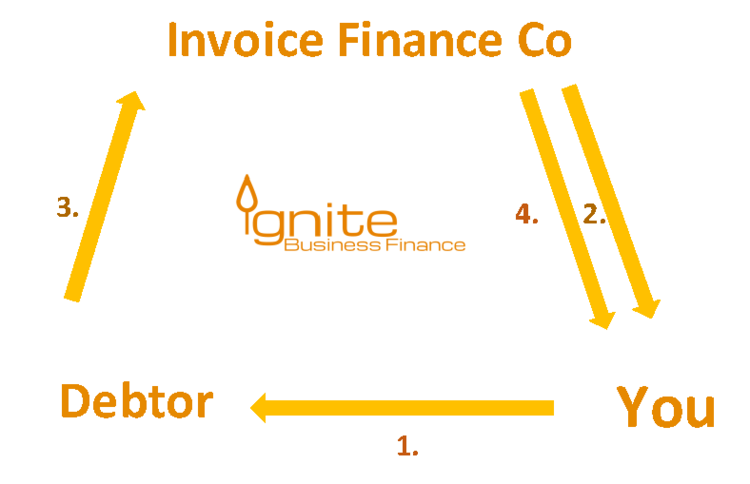

Invoice finance, also known as invoice factoring or accounts receivable financing, is a financial tool that allows businesses to leverage their unpaid invoices to access immediate working capital. It provides a solution for companies facing cash flow challenges due to the lag time between issuing invoices and receiving payment from customers. Instead of waiting 30, 60, or even 90 days for payment, businesses can essentially sell their invoices to a finance provider in exchange for a percentage of the invoice value upfront. The process typically involves these key steps: 1. **Invoice Generation:** The business provides goods or services to a customer and issues an invoice. 2. **Invoice Submission:** The business submits the invoice to the invoice finance provider. This can often be done electronically through a dedicated online platform. 3. **Advance Payment:** The finance provider verifies the invoice and advances a percentage of its value to the business. This advance, typically ranging from 70% to 90%, provides immediate access to working capital. 4. **Collection:** The invoice finance provider takes responsibility for collecting the payment from the customer. In some arrangements, known as recourse factoring, the business remains responsible if the customer fails to pay. In non-recourse factoring, the finance provider assumes the credit risk. 5. **Final Payment:** Once the customer pays the invoice, the finance provider remits the remaining balance to the business, minus their fees. These fees typically consist of a factoring fee, a discount fee, or a service fee, depending on the provider and the specific agreement. The benefits of invoice finance are numerous. It improves cash flow, enabling businesses to meet their immediate obligations, such as paying suppliers, salaries, and rent. By providing access to readily available funds, invoice finance also empowers businesses to take advantage of growth opportunities, such as investing in marketing, expanding operations, or accepting larger orders. Furthermore, invoice finance can streamline the accounts receivable process. By outsourcing the task of invoice collection to the finance provider, businesses can free up their internal resources to focus on core activities, such as sales and customer service. In non-recourse factoring, businesses are also protected from bad debt, as the finance provider assumes the risk of customer non-payment. However, it’s important to consider the potential drawbacks. The cost of invoice finance can be higher than traditional bank loans, particularly for businesses with strong credit histories. Furthermore, some businesses may be hesitant to cede control over their accounts receivable to a third party, especially if they have strong relationships with their customers. The perceived cost can also increase if the business fails to consider the lost opportunity cost of slow-paying customers. Before opting for invoice finance, businesses should carefully evaluate their needs and circumstances. They should compare the costs and benefits of different invoice finance providers and consider alternative funding options, such as bank loans or lines of credit. However, for businesses struggling with cash flow and seeking to accelerate growth, invoice finance can be a valuable and effective financial tool.

1858×984 generate invoice plugin purchase shop plugins from shopplugins.com

1858×984 generate invoice plugin purchase shop plugins from shopplugins.com  750×484 invoice finance prime finance from primefinance.co.nz

750×484 invoice finance prime finance from primefinance.co.nz  500×339 invoice finance sedge funding from sedgefunding.com

500×339 invoice finance sedge funding from sedgefunding.com  474×210 fast flexible invoice finance apply satago from www.satago.com

474×210 fast flexible invoice finance apply satago from www.satago.com  1024×683 invoice finance quick boost business cash flow from pacificfinance.com.au

1024×683 invoice finance quick boost business cash flow from pacificfinance.com.au  1080×608 invoice finance boost business cash flow octet from www.octet.com

1080×608 invoice finance boost business cash flow octet from www.octet.com  2000×1414 invoice generator from www.quickinvoicegenerator.com

2000×1414 invoice generator from www.quickinvoicegenerator.com  404×316 invoice generate projects logos illustrations from www.behance.net

404×316 invoice generate projects logos illustrations from www.behance.net  1349×972 generate invoice resume samples writing guides from zuryaraja.blogspot.com

1349×972 generate invoice resume samples writing guides from zuryaraja.blogspot.com  1748×1240 managing payroll invoice finance facility invoice financing from www.invoiceinterchange.com

1748×1240 managing payroll invoice finance facility invoice financing from www.invoiceinterchange.com  1200×630 invoices invoice generator from invoicegenerator.org

1200×630 invoices invoice generator from invoicegenerator.org  1200×630 build invoice generator easily from www.invoicepages.com

1200×630 build invoice generator easily from www.invoicepages.com  887×465 filefinancesgenerateinvoicepng voipms wiki from wiki.voip.ms

887×465 filefinancesgenerateinvoicepng voipms wiki from wiki.voip.ms  1230×526 invoice finance singapore read guide access invoice from www.tradefinanceglobal.com

1230×526 invoice finance singapore read guide access invoice from www.tradefinanceglobal.com  839×533 invoice generator create professional invoices from letsmakeinvoice.com

839×533 invoice generator create professional invoices from letsmakeinvoice.com  900×500 invoice finance benefits start businesses luv asset finance from luvassetfinance.co.uk

900×500 invoice finance benefits start businesses luv asset finance from luvassetfinance.co.uk  1119×940 invoice generator create invoice instantly from www.mooninvoice.com

1119×940 invoice generator create invoice instantly from www.mooninvoice.com  590×300 invoice creator easy generate invoices manage codemarket from code.market

590×300 invoice creator easy generate invoices manage codemarket from code.market  504×691 invoice generator zintego from www.zintego.com

504×691 invoice generator zintego from www.zintego.com  643×460 invoice generator systemx from www.systemx.net

643×460 invoice generator systemx from www.systemx.net  3315×6231 singapore invoice financing landscape invoice financing singapore from www.invoiceinterchange.com

3315×6231 singapore invoice financing landscape invoice financing singapore from www.invoiceinterchange.com  474×670 invoice maker singapore from www.invoicemaker.io

474×670 invoice maker singapore from www.invoicemaker.io  1024×576 singapore invoice generator template gst bullvoice business from www.bullvoice.com

1024×576 singapore invoice generator template gst bullvoice business from www.bullvoice.com  620×877 invoice generator create invoices invoice maker saldo apps from saldoinvoice.com

620×877 invoice generator create invoices invoice maker saldo apps from saldoinvoice.com  1600×1200 invoice generator santhosh thomas dribbble from dribbble.com

1600×1200 invoice generator santhosh thomas dribbble from dribbble.com  1600×1201 invoice inspiration muzli design inspiration from muz.li

1600×1201 invoice inspiration muzli design inspiration from muz.li  946×763 simple invoice app nz small businesses from www.soloapp.nz

946×763 simple invoice app nz small businesses from www.soloapp.nz  1920×1080 invoice financing platform smes invoice mate from www.invoicemate.net

1920×1080 invoice financing platform smes invoice mate from www.invoicemate.net  712×1284 create invoice template pertaining invoice template singapore from vancecountyfair.com

712×1284 create invoice template pertaining invoice template singapore from vancecountyfair.com  1786×2527 invoice templates freelancers billdu from www.billdu.com

1786×2527 invoice templates freelancers billdu from www.billdu.com